Indian Journal of Science and Technology

DOI: 10.17485/IJST/v14i31.1204

Year: 2021, Volume: 14, Issue: 31, Pages: 2557-2566

Original Article

Ganiyu A Busari1, Nae W Kwak2, Dong H Lim3*

1PhD. Student, Department of Bio & Medical Big Data, Gyeongsang National University, 501 Jinju-daero, Jinju, 52828, Republic of Korea

2Department of Information & Statistics, Statistics, Gyeongsang National University, 501 Jinju-daero, Jinju, 52828, Republic of Korea

3Professor, Department of Information & Statistics, Department of Bio & Medical Big Data

and RINS, Gyeongsang National University, 501 Jinju-daero, Jinju, 52828, Republic of Korea

*Corresponding Author

Email: [email protected]

Received Date:28 June 2021, Accepted Date:17 August 2021, Published Date:22 September 2021

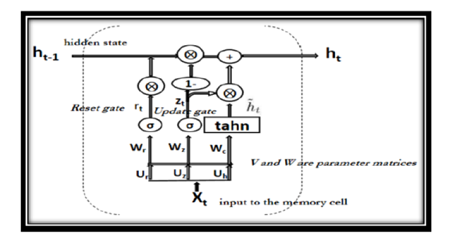

Objectives: Given the importance of accurate prediction of financial time series data and their benefits in the real-life, AdaBoost-GRU ensemble learning is proposed in which it’s forecasting accuracy is to be compared with AdaBoost-LSTM, single Long Short Term Memory (LSTM), and single Gated Recurrent Unit (GRU). Methods: The data for Korea Composite Stock Price Index (KOSPI) obtained from Naver Finance from January 2000 to April 2020, the Oil Price data for the entire Gyeongnam region among domestic oil price data obtained from Korea Petroleum Corporation (Opinet) and USD Exchange data provided by Naver Financial from April 2004 to May 2020 were employed. The analyses were made using mean absolute error (MAE), mean squared error (MSE) and root mean squared error (RMSE) as the performance metric. Findings: Empirical results show that the proposed method outperforms all other models that serve as benchmarked models, in all three kinds of data used in this research. This also shows that ensemble models have better performance than the single models as both AdaBoost-GRU and AdaBoost-LSTM outperform their respective single GRU and single LSTM. Novelty/Applications: This empirical study suggests that the AdaBoost-GRU ensemble-learning model is a highly promising approach for forecasting these kinds of data. However, another ensemble model that can combine AdaBoost with other single models such as ConvD1 can be developed and applied.

Keywords: Oil Price; Exchange Rate; Stock Price Index; Time Series Forecasting; AdaBoost Algorithm; Gated Recurrent Unit

© 2021 Busari et al. This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited. Published By Indian Society for Education and Environment (iSee)

Subscribe now for latest articles and news.